American Express does something that no other credit card issuer really does. When you apply for certain Amex cards, they'll show you a personalized welcome bonus before you actually commit to the application. They call it an "as high as" offer, and the best part is that checking your offer only triggers a soft credit pull. If you don't like what you see, you can walk away with zero impact to your credit score.

Here's how it works, which cards currently have "as high as" offers, and what you should expect when you apply.

What Is an "As High As" Offer?

Most credit card issuers give you a set welcome bonus. Apply for the card, hit the spending requirement, get your points. Simple. American Express takes a different approach with certain cards.

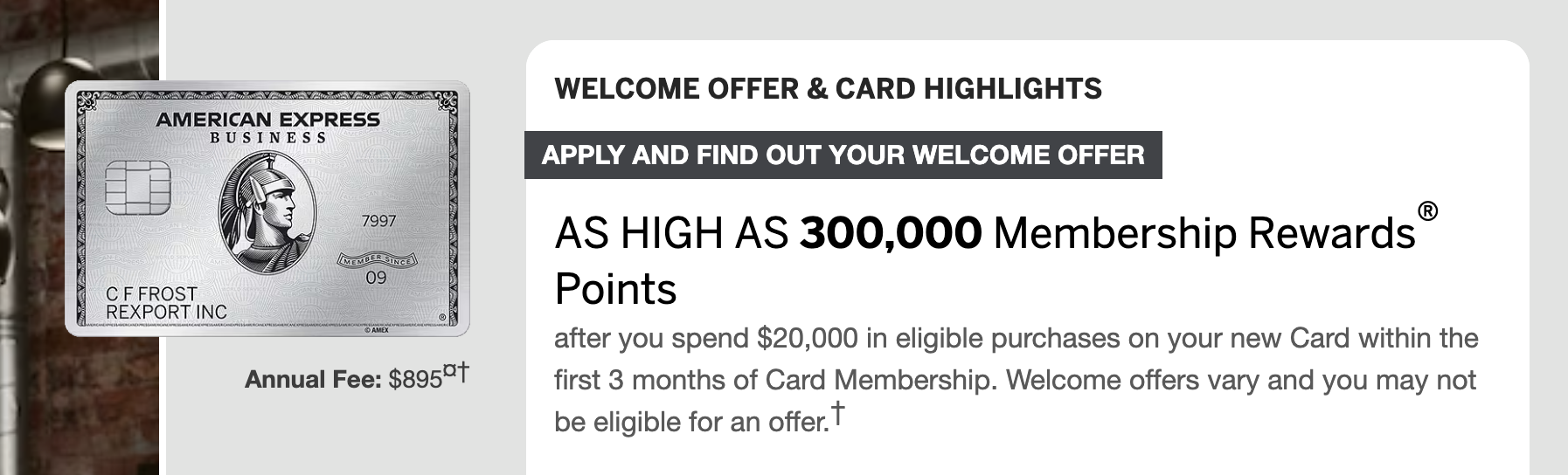

Instead of advertising one fixed bonus, Amex shows the top range of what you could get. So you'll see something like "earn as high as 300,000 Membership Rewards points." That 300,000 is the ceiling, not a guarantee. Your actual offer could be anywhere from the minimum to that top number, depending on what Amex decides you qualify for.

The key difference here is that you get to see your personalized offer before Amex does a hard pull on your credit. You fill out the application, Amex runs a soft credit check, and then they present you with your actual bonus number. At that point, you choose whether to move forward or not.

Key Takeaway: "As high as" means the advertised number is the maximum possible bonus. Your actual offer may be lower, and you won't know until you submit your info for a soft pull.

How the Application Process Works (Step by Step)

This is where it gets interesting, and where a lot of people get confused. Here's exactly what happens when you apply for a card with an "as high as" offer.

Step 1: Click Through an "As High As" Link

You'll find these offers through various links online. When you click "Apply Now," you'll land on a page that shows the top range, something like "as high as 300,000 Membership Rewards points."

Using one of the links below to apply supports my work.

Step 2: Fill Out the Application

You go through the standard application process. Name, address, income, the usual stuff. Nothing different here from any other credit card application.

Step 3: Submit to See Your Offer (Soft Pull Only)

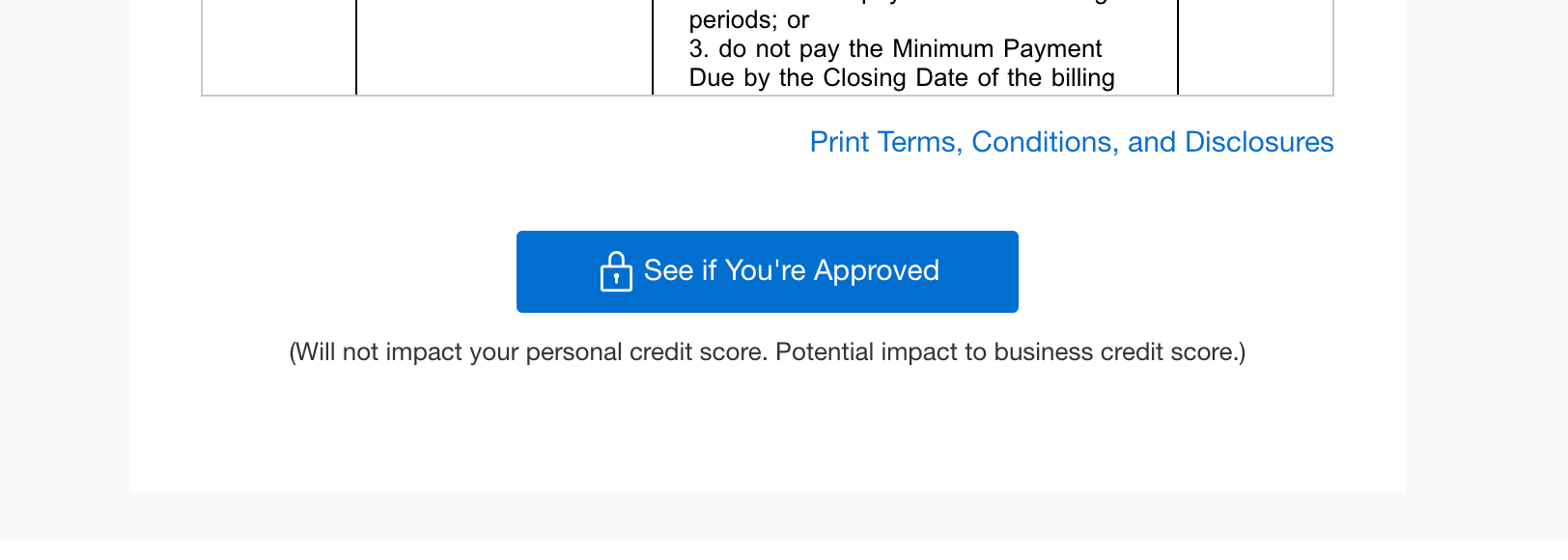

Here's the important part. When you click submit, Amex does a soft credit pull to determine your eligibility. Right below the submit button, you'll see a note that says something like "welcome offers vary, and you may not be eligible for an offer. This will not impact your personal credit score or business credit score."

That's Amex telling you upfront: this step is risk-free. No hard pull. No impact on your credit.

Step 4: View Your Personalized Offer

After the soft pull, Amex shows you your actual bonus. This is your personalized welcome offer based on whatever criteria Amex uses behind the scenes.

For example, you might click through an "as high as 300,000 points" offer and get presented with 150,000 points. Not the 300,000 you saw advertised, but 150,000 is still a solid bonus.

Step 5: Accept or Decline

Now you decide. If you're happy with the offer, you click "See if You're Approved" and that's when Amex does a hard pull on your credit. This is the point where your credit score could potentially be affected.

If you're not happy with the offer, you can decline and walk away. No hard pull. No credit impact. No harm done.

What If You Get a Lower Offer?

Let's say the Amex Gold is advertising "as high as 100,000 points." You go through the process and get offered 50,000 points. You have two options:

Option 1: Accept the 50,000 point offer. Amex does a hard pull, processes your application, and you move forward. 50,000 Amex points is still worth a solid amount depending on how you use them.

Option 2: Decline the offer. No hard pull happens. Your credit score stays untouched. You can try again later or look for a different offer link.

This is honestly one of the best things about the "as high as" system. You get to make an informed decision with actual numbers before committing, and the only cost of checking is a soft pull that nobody can see but you.

Why Your Offer Might Be Different

Amex hasn't publicly shared exactly how they determine who gets what offer. But a few things likely play a role: your credit profile, your existing relationship with American Express, how many Amex cards you already have, and potentially the specific link you used to access the application.

Bottom Line

American Express "as high as" offers let you see your personalized welcome bonus with only a soft credit check. If you like the offer, you proceed and Amex does a hard pull. If you don't like it, you decline with zero impact to your credit score. Four cards currently use this system: the Amex Gold, Amex Platinum, Amex Business Gold, and Amex Business Platinum.

The process is simple: apply, see your offer (soft pull), then decide whether to accept (hard pull) or walk away (no impact). It takes the guesswork out of the application process, and that's a win.

Using one of the links below to apply supports my work.