Chase just added World of Hyatt Explorist status to the Chase Sapphire Reserve. Starting April 1st, 2026, Sapphire Reserve cardholders who spend $75,000 in a calendar year will earn Explorist status. For the Sapphire Reserve business card, the threshold is $125,000.

It sounds like a major upgrade. It's not. And if you're planning to stack $75,000 in spend on your Chase Sapphire Reserve to unlock it, you're leaving serious value on the table.

What You Actually Get With Explorist Status

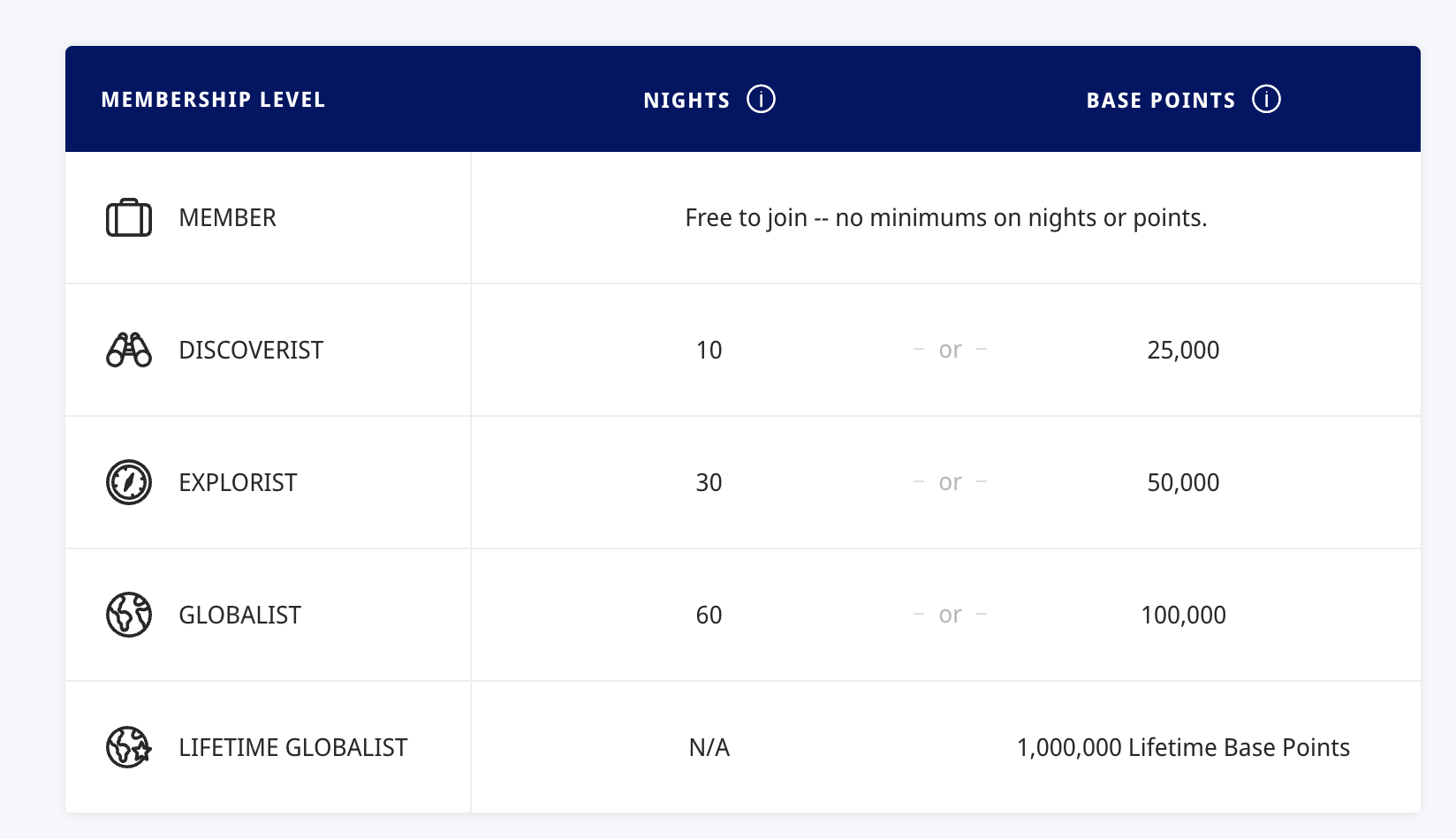

Explorist is the middle tier in Hyatt's loyalty program. The full ladder goes Discoverist (10 qualifying nights), Explorist (30 qualifying nights), and Globalist (60 qualifying nights).

Explorist comes with a 20% bonus on base points, complimentary premium internet, room upgrades excluding suites and club rooms (subject to availability), and late checkout until 2 p.m. when available.

It's a nice set of perks. It's not going to change how you travel.

This new benefit stacks on top of the other CSR tier rewards at $75,000 in annual spend: IHG One Rewards Diamond status, Southwest Airlines A-List status, and a $500 Southwest Airlines credit through Chase Travel.

The Math: $75,000 on the CSR vs. the Hyatt Credit Card

The Chase Sapphire Reserve earns 1x on general spending. Unless you're hitting the 3x dining or 3x travel categories, every dollar of that $75,000 earns you a single Chase Ultimate Rewards point.

Put that same $75,000 on the World of Hyatt credit card and the math looks completely different.

The Hyatt personal card earns 2 qualifying nights toward elite status for every $5,000 in spend. At $75,000, that's 15 cycles times 2, giving you 30 qualifying nights from spend alone. Add the 5 qualifying nights you get just for holding the card, and you're at 35 qualifying nights total.

Explorist requires 30 nights. You hit the exact same status either way. The difference is everything that comes with the Hyatt card path.

The Milestone Rewards Make It a No-Brainer

Hitting qualifying night milestones on the Hyatt card unlocks reward choices that don't exist on the CSR path.

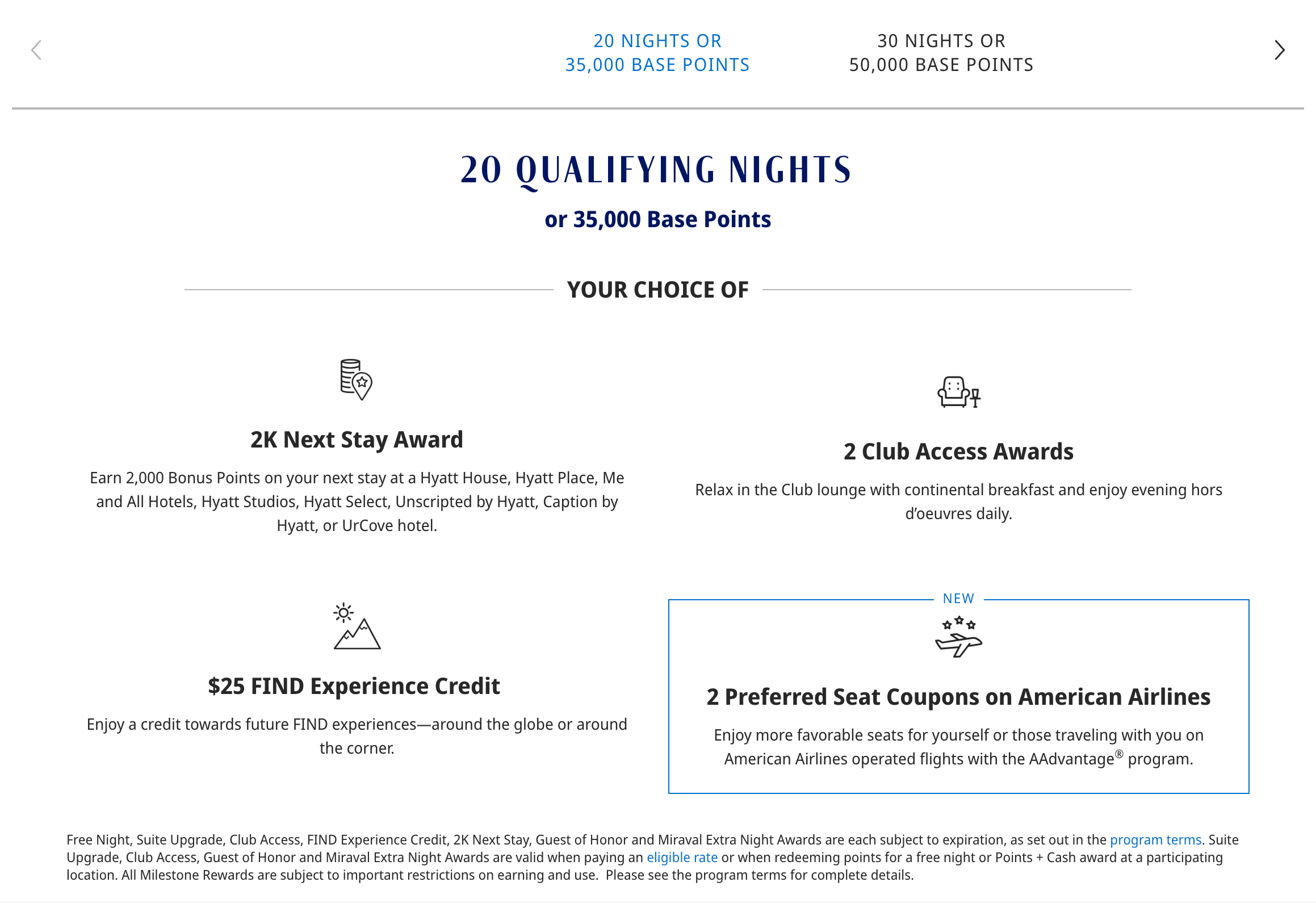

At 20 qualifying nights, you pick one: 2,000 bonus Hyatt points on your next stay at a Hyatt House, Hyatt Place, or Caption by Hyatt , 2 club lounge access awards, a $25 Find experience credit, or 2 preferred seat coupons on American Airlines.

The 2,000 bonus points are the move at this tier.

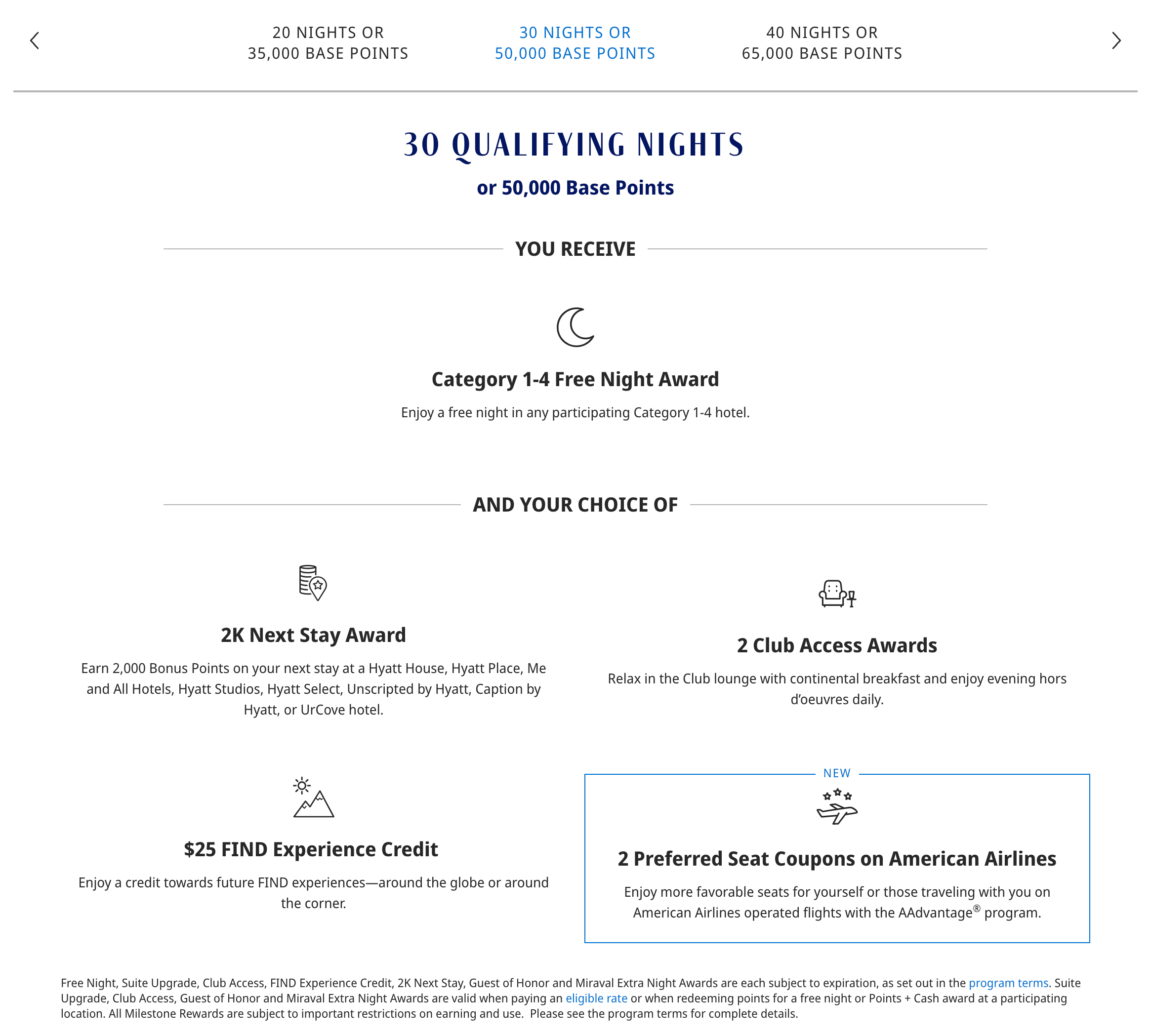

At 30 qualifying nights, which you'll hit with $75,000 in spend, you earn a category 1 through 4 night award. That's a hotel night worth up to 15,000 Hyatt points. Plus another choice from the same milestone menu.

And when you spend $15,000 on the Hyatt card in a calendar year, you earn another category 1 through 4 night award on top of everything else.

So at $75,000 on the Hyatt card, you're walking away with Explorist status, 35 qualifying nights toward Globalist, two category 1-4 night awards, milestone reward picks, and all the Hyatt points from your spend. Put that same $75,000 on the CSR? You get Explorist. That's it. Well, you do get a few more perks, but they are not Hyatt-related. More on that below.

Key Takeaway: Both cards earn you Explorist at $75,000 in spend. The Hyatt card also earns you milestone rewards, night awards, and puts you more than halfway to Globalist. The CSR gives you the status and nothing else on the Hyatt side.

The Case for the CSR Quadruple Dip

I'll give the CSR credit where it's earned. At $75,000 in spend, you're not just getting Hyatt Explorist. You also unlock IHG Diamond elite status, Southwest A-List status, and a $500 Southwest credit through Chase Travel.

If you genuinely value all four of those programs, that's a quadruple dip that the Hyatt card can't match.

You have to ask yourself though: is a quadruple dip on mid-tier status across four programs better than going deep on the one program you actually use? For most Hyatt loyalists, the answer is no.

Why Chase Keeps Losing to Amex

This Hyatt Explorist perk fits a pattern. Since the Chase Sapphire Reserve relaunched last year, Chase has been piling on benefits. The select hotel credit through Chase Travel. The Whoop credit. Now Hyatt Explorist at $75K. When a card company keeps throwing perks at a product, it tells you people aren't as excited about it as they'd like.

The reason is pretty clear. Compare the credits on both cards.

The Amex Platinum makes it easy. The Lululemon credit? Activate it, go buy something at Lululemon. The Walmart Plus credit? Sign up for Walmart Plus, it's covered. The Resy credit? Dine at a Resy restaurant. The Uber credit? Add your Platinum to your Uber account and Uber cash gets deposited into your account every single month. Simple, straightforward, obvious value.

Now look at the Chase Sapphire Reserve. The $300 DoorDash promo is broken into $25 per month. And that $25 is split further into $5 for restaurant orders and two $10 promos for groceries and retail. So it's $10, $10, and $5 every month. That's already confusing. The StubHub credit is $150 in the first half of the year and $150 in the second half, not monthly, biannually. And I've heard a lot of bad experiences trying to actually use it. The OpenTable dining credit requires the restaurant to be part of the Sapphire Table program on OpenTable, and the restaurant network isn't that big.

Every CSR benefit comes with another hoop to jump through. Another restriction. Another layer of fine print. People understand coupons. That's the new normal for premium credit cards. Everybody has credits and perks built into their cards now. The difference is how easy they are to actually use. Amex makes the value obvious. Chase makes you work for it. And that's why the Platinum keeps pulling people away from the Reserve.

Why 2026 Is Still a Good Year to Get the CSR

With all that said, I still think the Chase Sapphire Reserve is worth picking up in 2026.

The sign-up bonus right now is 125,000 Chase Ultimate Rewards points after $6,000 spent in the first 3 months. That's about $2,000 a month in spend, which is reasonable. Compare that to the Amex Platinum's current minimum of $12,000 in 6 months. Same monthly rate, but $12,000 total is a reach for a lot of people. I'm working on two minimum spend requirements right now between two different cards and even for me it hasn't been easy.

The CSR also comes with the new select hotels credit for 2026, which stacks with the other credits to offset the annual fee in year one. Between the sign-up bonus, the stacking credits, and the reasonable minimum spend, the value proposition is strong right now.

Get the card for the bonus and the credits. Just don't put $75,000 on it chasing Hyatt Explorist when the Hyatt card does it better from day one.

Bottom Line

If you want Hyatt status, get the Hyatt credit card. Put your spend there, earn toward Globalist, and collect milestone rewards along the way. At $75,000 in spend you're hitting Explorist and sitting at 35 qualifying nights, more than halfway to the top tier.

If you want the Chase Sapphire Reserve, get it in 2026 for the 125,000-point bonus and stack the credits. It's still a solid card. Just not the right tool for earning Hyatt status.